This website is for the use of FCA authorised mortgage intermediaries only.

Application Help Centre

Keying an application right first time

The below information will assist you with inputting the application onto our Broker platform and includes information about common keying errors.

Following this guidance can also help reduce the likelihood of an incorrect system decline decision, and ensure that the application is progressed as quickly as possible.

Top 5 keying errors

BTL / Second home costs

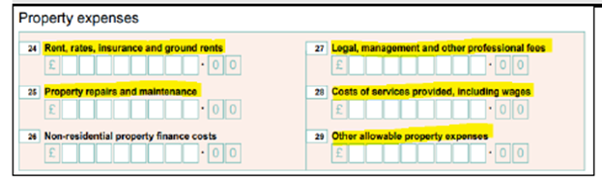

HSBC UK does not consider BTL self-financing and require all mortgages and running costs to be included even where the property is partially owned. These can be taken from the SA100 and added to the application:

- Rent, rates, insurance and ground rents

- Property repairs and maintenance

- Legal management and other professional fees

- Costs of services provided, including wages

- Other allowable property expenses

Where an SA100 has not been submitted as the property has been owned for less than 18 months, running costs such as utilities, insurance, council tax need to be included.

This is to cover periods where the property may be untenanted. If the BTLs are held in a Limited Company, the BTL expenditure for these properties does not need to be included.

For applications with properties in the background such as second homes, we need to include any background running costs for the second home within expenditure, even where the property will be occupied by other family members.

These running costs include council tax, utilities, insurance. Mortgages should be included if they appear on the customer’s credit report, this includes where they are held jointly with siblings, children, etc.

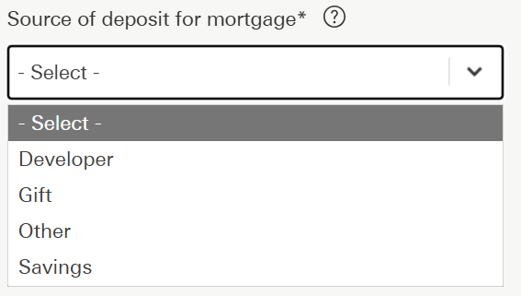

Deposit

Standard applications:

- When completing a Home mover application, where the deposit is ‘Equity’, please select ‘Other’.

- Where selecting ‘Other’ as source of deposit, please add a note to confirm the origin of funds and whether the current property is being sold or retained.

Foreign national / Overseas applications:

- For Foreign national / Overseas applicants, if the deposit is coming from sale of property, it should be keyed as ‘Savings’.

- A common error is the deposit being keyed as ‘Other’ with a description of ‘sale of property’. This causes the DIP to decline for not meeting our Foreign national / Overseas deposit criteria.

- In the above scenario, please add notes to the case to confirm exactly where the source of deposit originates from.

Duplicate applications

Where an offer is going to expire before completion, please ensure the case is cancelled before submitting a new application. This will prevent issues at drawdown.

Leasehold costs

We use modelled expenditure based on the property to be mortgaged for many essential expenditure items, so these do not need to be separately input into the application. The following however need to be included:

- For all leasehold properties – ground rent / service charge, and any associated costs, must be included.

- Travel:

- Essential travel including any costs associated with the commute to work (e.g. fuel, parking, public transport fares)

- Costs associated with running a vehicle (e.g. insurance / tax / service / maintenance costs)

- Payslip deductions (e.g. season ticket loan / Cycle to Work / car lease / car parking)

- Childcare – as well as including any regular costs, please include any childcare vouchers

- School / Further or Higher Education fees need to be included, even where savings or family members will cover the cost.

Providing payslips

- If the employer’s registered address differs from the employer’s address shown on the payslip, please add a note to explain the discrepancy

- If the customer’s address on the application differs from payslip, please add a note to explain the discrepancy

- Where there is a difference with the customer’s name on the application to that shown on the payslip (e.g. maiden name / married name), please upload the marriage certificate

- Payslip validity: Where the payslip includes both a date the payslip is issued and a pay date, the 35-day validity period is calculated from the pay date. For example, if a wage slip covers the period from 1st February to 28th February, but the pay date is listed as 25th February, the pay date (25th February) should be used as the reference point

- If there is a variance in multiple payslips showing differing basic pay / hours, please add a note to explain if this is zero-hour contract / fixed term contract etc.

Applicant

Application type and rates

Buyer types and rates - hints and tips

To ensure applications are keyed correctly and the appropriate rate is chosen, please review the below hints & tips.

If the application is incorrectly keyed, or the wrong rate selected, this can result in case delays or rekeying of cases.

Additional borrowing:

For Additional borrowing applications, please select ‘Existing Customer Borrowing More’ rates.

Porting:

For Porting customers who are also increasing their borrowing amount, please select ‘Home Mover’ rates.

First time buyers:

First time buyers are defined as: ‘At least one applicant has never previously owned a property in the UK or abroad’. If the applicant doesn’t meet this criteria, an alternative rate should be chosen.

Premier rates:

Only applicants who hold an HSBC Premier account are eligible for these rates. Once the case is at submission, the underwriter will check whether the applicants are eligible against HSBC internal systems.

Energy Efficient Homes Cashback (EEHC) rates:

See Energy efficient homes section.

International rates:

A non-UK resident in an approved country must select an International rate.

Premier / Tracker rates:

When keying the application, if only Premier / Tracker rates are showing, please review the selected incentives (e.g. Cashback / Fee Assisted). If the issue is not resolved, please contact our Broker Support helpdesk.

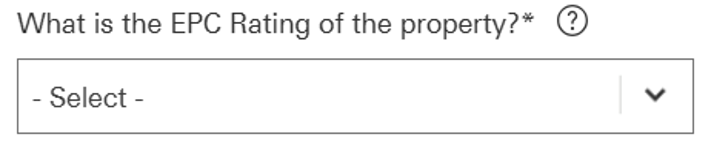

Energy efficient homes and EPC

The Energy Efficient Home Cashback (EEHC) mortgage product rewards customers who purchase a more energy efficient home.

Cashback is received for Residential customers purchasing or remortgaging to HSBC UK with a home that has an Energy Performance Certificate (EPC) rating of A or B.

- If no EPC has been carried out, or the customer has not yet found a property, ‘Expired / Unknown’ needs to be selected.

- If the property is under construction, the broker must provide a Predicted Energy Assessment (PEA) certificate.

The PEA certificate will be provided by the developer (and should contain the address or proposed address of the property, if the PEA certificate does not cover the above, a Plot Reservation form will also be required).

- Only properties with EPC / PEA rating of A or B are eligible for EEHC rates (Purchase / Remortgage applications up to £2,000,000).

- Unencumbered properties, Additional borrowing, Product switches and Buy to let properties are not eligible for EEH rates.

Help to buy

We are able to accept a Remortgage application with Additional borrowing to repay a Help to Buy loan. The application needs to be keyed as a multi part loan, one part to repay the existing mortgage and one part for the new monies to purchase the final share.

Porting keyed as purchase

If a Porting application is keyed as a Purchase application, the system doesn’t pull through the customer’s existing HSBC UK mortgage details.

- Select ‘Existing customer’ from the broker dashboard.

- Details must be input and exactly match those already held on HSBC systems.

- If keyed incorrectly, a Purchase application cannot be amended to a Porting application and a new application will need to be submitted.

Product switching and Additional borrowing

We allow Product switch and Additional borrowing applications to take place at the same time. You will need to input these requests as two separate applications.

If the product rate selected on the Product switch and Additional borrowing application are the same, one fee is fully refundable. However, where the products are not the same, a booking fee applies to each fee-paying product.

You will need to contact our Broker Support helpdesk when one of the booking fees is eligible for a refund; the request must be made before the application completes.

We classify applications to be simultaneous when they are keyed within three working days of each other. Please ensure that booking fees are not capitalised if a refund is required.

If you are submitting a Product switch and an Additional borrowing application for the same customers, please be aware that if the Product switch application completes before the Additional borrowing decision has been given, your customer will be required to pay an early repayment charge if the Product switch application is subsequently cancelled.

Key points for refund of booking fee:

- Input as two separate applications – must be keyed within three working days of each other.

- The broker must select the same rate for both applications to be eligible for a refund of one of the fees.

Keying Option 1 (preferred):

- Booking fees paid up front on both Product switch and Additional borrowing applications.

- Broker to contact helpdesk to notify us that a refund is required immediately after the applications are submitted.

- A refund will be actioned on the Additional borrowing application.

Keying Option 2:

- Booking fee paid up front on Product switch application only and capitalised on the Additional borrowing.

- Broker to upload AAF (to the Additional borrowing application) immediately after the applications are submitted to request the Additional borrowing quote be amended to remove the fee.

Remortgage applications - rate incentives

Products including cashback:

This will be instructed as General Panel Managed (the customer will need to select their own Solicitors firm from our panel and will pay the fees).

Products including Fee Assisted Legals:

This will be instructed as Fees Assisted and a firm will be allocated from our panel to act (the customer does not choose the Solicitors firm here).

Products with no incentives:

This will be instructed as General Panel Managed (so the customer will need to select their own Solicitors firm from our panel and will pay the fees).

Products with cashback and Fee Assisted Legals:

This would only apply to EEHC rates (so the property would need to fit the guidelines for an Energy Efficient rate) – this would be instructed as Fees Assisted and the Solicitors firm will be panelled out to act (the customer does not choose the Solicitors firm here).

Please note that any incentives are paid per application not per product.

Employment / income

Current employment details

- Please select the employment status as accurately as possible.

- If the applicant’s start date is less than six months ago, a copy of the contract of employment may be required.

- For joint applications where the second income is not required to support affordability, the current employment status should still be input (with £0 income).

‘Are you on a Zero Hours contract or Fixed Term contract?’

- For Agency or Short / Fixed term contract workers, please select ‘Yes’ to this question.

‘Is the applicant aware of any future changes to their income and expenditure?’

- Please tick ‘Yes’ to this question if there are any expected changes to the customer’s income including redundancies, change of roles and maternity leave.

- For maternity leave, please also include future childcare costs and any changes to the applicant’s income / terms of work.

- The Parental Leave form must be uploaded to the application.

- Please input employer’s name as displayed on the payslip. Incorrect details can lead to further questions and delays in the application journey.

Employers address

Please key the customer’s employer / business address as accurately as possible.

- As part of our underwriting checks, we undertake a sensibility check on all travel costs, and compare these to the employer’s address.

- If you are inputting an address which is head office or a site where the customer does not work from, please detail this at the end of the application in the notes section. This includes working from home, hybrid working, etc.

Other income

Benefit income

- Benefit income can only be used where these are evidenced to be assured and regular and will be received over the full term of the mortgage.

Rental income

- The monthly rental income keyed should be the gross rental income as evidenced by the SA100. Please note, even if you are not using Buy to let income, all associated costs still need to be included in the application.

- If the applicant is considered a Portfolio Landlord (including BTLs in holding companies), rental income cannot be used and must be excluded from affordability.

Retirement age

- Please complete both applicants’ anticipated retirement age.

- Where retirement age is declared as above 70, the system will automatically base affordability up to the age of 70 as a prepopulated retirement age.

Providing payslips

- If the employer’s registered address differs from the employer’s address shown on the payslip, please add a note to explain the discrepancy

- If the customer’s address on the application differs from payslip, please add a note to explain the discrepancy

- Where there is a difference with the customer’s name on the application to that shown on the payslip (e.g. maiden name / married name), please upload the marriage certificate

- Payslip validity: Where the payslip includes both a date the payslip is issued and a pay date, the 35-day validity period is calculated from the pay date. For example, if a wage slip covers the period from 1st February to 28th February, but the pay date is listed as 25th February, the pay date (25th February) should be used as the reference point

- If there is a variance in multiple payslips showing differing basic pay / hours, please add a note to explain if this is zero-hour contract / fixed term contract etc.

Self-employed - Limited Co director - shareholder

When completing employer details for Self-employed Limited Company Director / shareholder:

- Please ensure the Director’s salary is included in the correct field.

- If there is no Director’s salary, please input £0 for both the latest and previous years, as this can cause the DIP to decline if left blank.

- If the company is a trading company and there is a holding company involved, please provide their latest year’s finalised financial accounts along with the trading companies latest year’s finalised financial accounts.

Expenditure

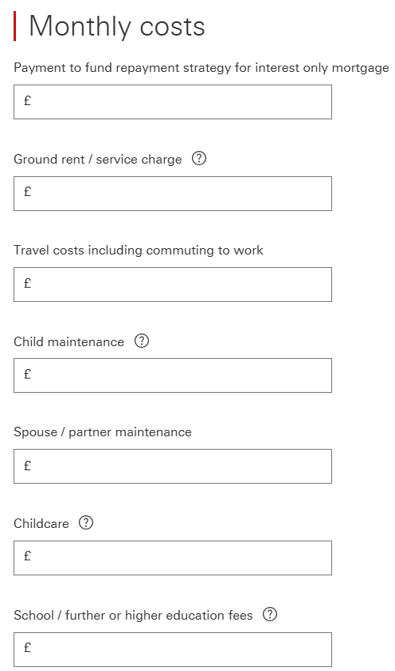

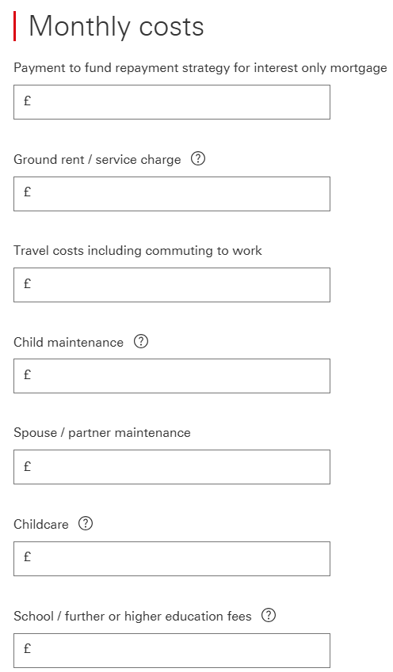

Ad-hoc capital as repayment plan for Interest only mortgage included in expenditure

When the repayment plan for Interest Only is ad-hoc capital, this should be input into ‘Regular Outgoings’ as ‘Payment to fund repayment strategy for Interest Only mortgage’ so the system does not include this as an existing commitment.

If the Ad-hoc payment is entered under any other ‘Regular Outgoing’ – e.g. ‘Other Outgoings’ – the system will include this as an expenditure.

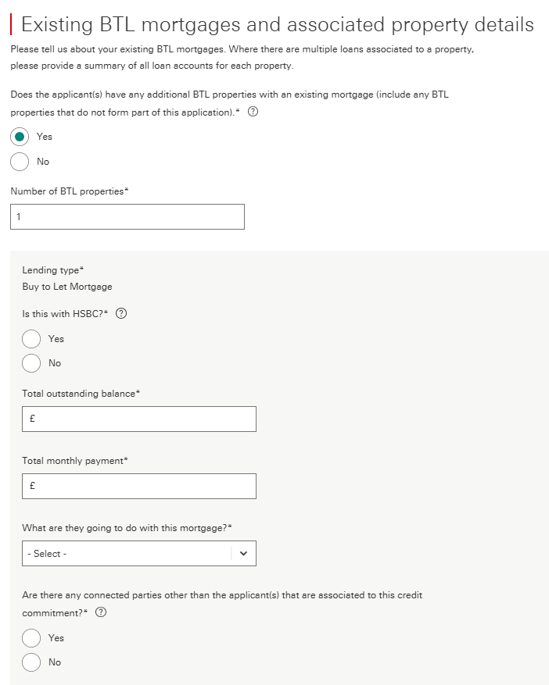

Buy to let costs (BTL in the background)

HSBC UK does not consider BTL self-financing and require all mortgages and running costs to be included even where the property is partially owned. These can be taken from the SA100 and added to the application:

- Rent, rates, insurance and ground rents

- Property repairs and maintenance

- Legal management and other professional fees

- Costs of services provided, including wages

- Other allowable property expenses

Where an SA100 has not been submitted as the property has been owned for less than 18 months, running costs such as utilities, insurance, council tax need to be included.

This is to cover periods where the property may be untenanted. If the BTLs are held in a Limited Company, the BTL expenditure for these properties does not need to be included.

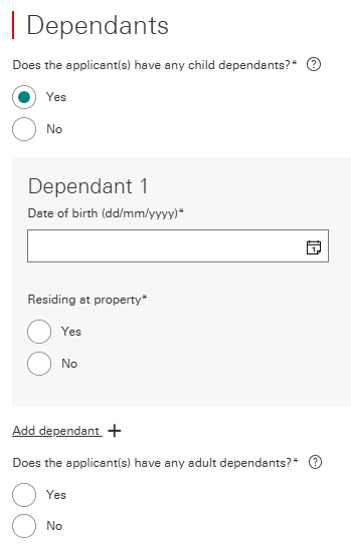

Dependants

Please key the dependant’s date of birth as accurately as possible as this can cause delays to the application.

- Incorrectly keying the date of birth can lead to further questions by the underwriter regarding childcare costs.

- Anyone aged 17 or older at the time of the application submission, who lives in the property but is not on the mortgage application (excluding full-time students), will be required to sign a Letter of Consent.

Adult Dependants: An adult dependant is defined as any member of the applicant’s immediate family who is:

- Financially dependent on the applicant

- Over the age of 18

- Not included on the mortgage, but living with the applicant full time

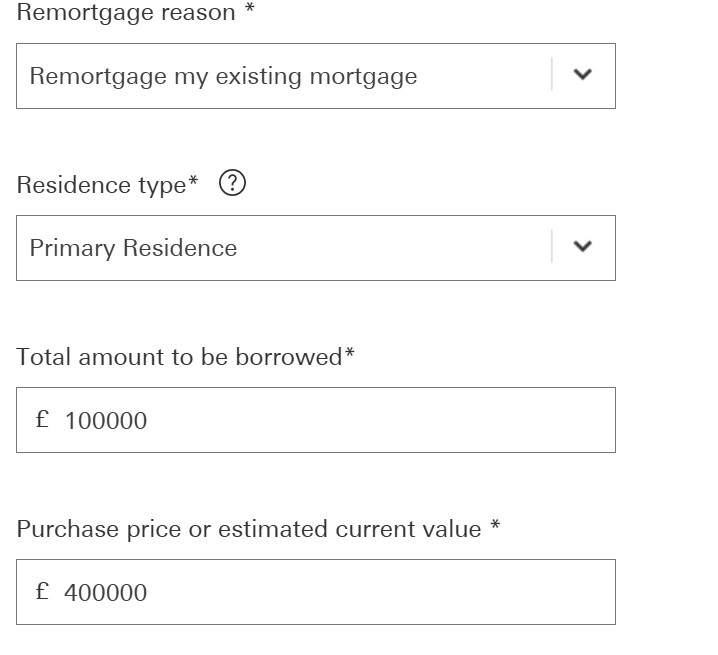

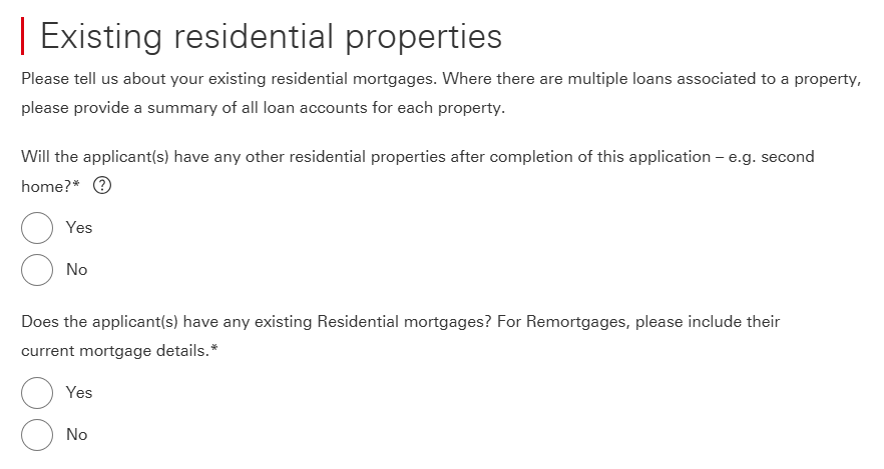

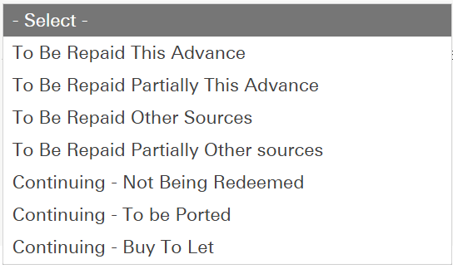

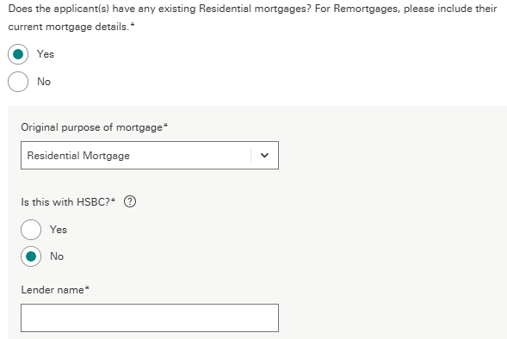

Exisiting Residential mortgages - how to key

For Purchase and Porting applications, if ‘Yes’ is answered to the question ‘Does the applicants have any existing Residential mortgages?’, the application will continue to ask, ‘What are they going to do with this mortgage?’

If the applicants are repaying their existing mortgage and completing their HSBC UK mortgage simultaneously, the broker needs to select ‘To Be Repaid This Advance’.

Any other selection will result in the mortgage payment amount being retained as a commitment.

A common scenario where we see applications declining is where the external residential mortgage is being repaid upon completion and has been keyed as ‘To Be Repaid Other Sources’.

This should be keyed as ‘To Be Repaid This Advance’. For Remortgage applications, this section is automatically completed as ‘To Be Repaid This Advance’.

Where an applicant is repaying their existing mortgage simultaneously with completing the HSBC UK mortgage application, the answer to the question ‘What are they going to do with this mortgage?’ should be ‘To Be Repaid This Advance’.

Any other choice will result in the existing mortgage payment being included in expenditure.

The most common issue seen is the option ‘To Be Repaid Other Sources’ instead of ‘To Be Repaid This Advance’ being selected. Remortgage applications will automatically default to the option of ‘To Be Repaid This Advance’.

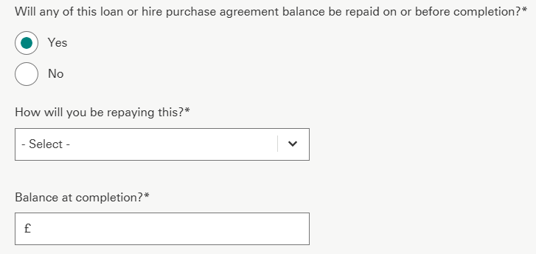

Financial commitments - debts to be repaid upon completion

Although the system allows you to record any debts which will be repaid upon completion, these still need to be included in the affordability calculator to provide an indicative maximum lend. This also includes inputting any credit cards which are repaid in full each month.

- Always include the lender’s name as accurately as possible to prevent delays in the application journey. Debts that will expire in less than six months can be excluded from the affordability calculation.

- Common errors - Even if existing debts are to be repaid upon completion, they still need to be included in the expenditure to provide an indicative maximum lending figure.

- The system shows fields which allow you to record any debts that will be repaid upon completion; however, they must still be included in the affordability assessment, including any credit cards that are repaid in full each month.

Household expenditure

We use modelled expenditure based on the property to be mortgaged for many essential expenditure items, so these do not need to be separately input into the application. The following however need to be included:

- For all leasehold properties – ground rent / service charge, and any associated costs, must be included.

- Travel:

- Essential travel including any costs associated with the commute to work (e.g. fuel, parking, public transport fares)

- Costs associated with running a vehicle (e.g. insurance / tax / service / maintenance costs)

- Payslip deductions (e.g. season ticket loan / Cycle to Work / car lease / car parking)

- Childcare – as well as including any regular costs, please include any childcare vouchers

- School / Further or Higher Education fees need to be included, even where savings or family members will cover the cost.

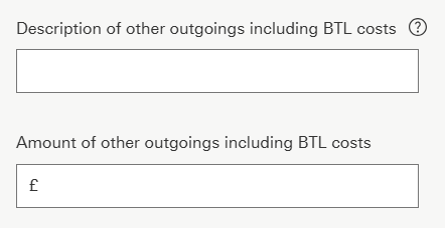

Household expenditure - other

All other non-credit commitment costs which aren’t captured within the DIP need to be included in ‘Other outgoings’. The below list is not exhaustive, but does give an example of what may need to be included in the affordability assessment:

- Buy to let costs

- Second home costs

- Overseas property expenditure (including mortgages and running costs)

- Payslip deductions including employer loan, armed forces accommodation, Credit Union, etc.

- Guarantor mortgages. If the customer is guarantor for a mortgage they are not named on, they may still be liable for this cost.

Lender name left blank

When keying existing external mortgages into the application, if the existing lenders name is left blank, this can cause the DIP to decline.

Second residential incorrectly keyed

This only relates to second properties – retained / additional properties, not a remortgage.

If an application is incorrectly keyed as a second residential which will remain upon completion, the system will restrict the maximum LTV for the second property at 80%.

- On the Existing Residential Properties section of the application the system asks, ‘Does the applicant own any other residential properties?’

- This question relates to how many residential properties the applicants will own upon completion.

- For applications with properties in the background such as second homes, we need to include any background running costs for the second home within expenditure, even where the property will be occupied by other family members.

- These running costs include council tax, utilities, insurance. Mortgages should be included if they appear on the customer’s credit report, this includes where they are held jointly with siblings, children, etc.

- If an existing property is being sold or converted as part of the new purchase application, then the answer to the questions ‘Does the applicant(s) have any other residential properties remaining in the background – e.g. a second home?’ and ‘Does the applicant(s) have any existing Residential mortgages?’ should be ‘No’.

- Keying the application with a second residential property will restrict the maximum LTV to 80%.

- The 80% LTV restriction will also be applied if the ‘Residence type’ field is populated with Secondary Residence.

Top slicing applications

When completing the Top slicing calculator, where a residential mortgage is held in joint names, please key this under applicant 1 only. Do not key ‘0’ or any text in the residential mortgage field for applicant 2 as this can affect the indicated maximum loan result.

Property

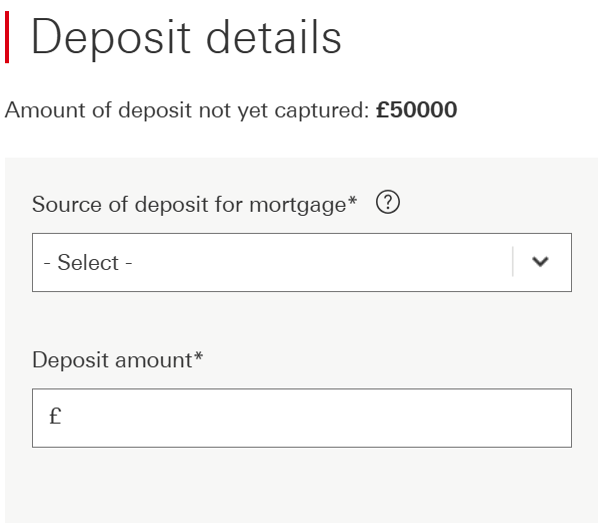

Deposit

Standard applications:

- When completing a Home mover application, where the deposit is ‘Equity’, please select ‘Other’.

- Where selecting ‘Other’ as source of deposit, please add a note to confirm the origin of funds and whether the current property is being sold or retained.

Foreign national / Overseas applications:

- For Foreign national / Overseas applicants, if the deposit is coming from sale of property, it should be keyed as ‘Savings’.

- A common error is the deposit being keyed as ‘Other’ with a description of ‘sale of property’. This causes the DIP to decline for not meeting our Foreign national / Overseas deposit criteria.

- In the above scenario, please add notes to the case to confirm exactly where the source of deposit originates from.

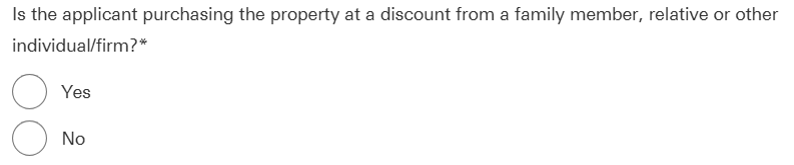

Discounted properties

- If a discount has been applied to the property by family members, relatives or any other individuals / firm, please select ‘Yes’ to this question.

- Loan to value, for policy, is linked to the ‘actual’ purchase price being paid to purchase the property. The customer’s minimum deposit must be in line with criteria linked to this LTV.

- The correct way to key this type of application is the following:

- Submit the case based on the actual market value of the property. This way, the valuation is instructed on the correct value and the correct rate can be selected.

- Upload an Application Amendment Form to change the purchase price to reflect the discounted amount that the property is being purchased for.

Please note, this needs to remain within policy limits for loan to value (LTV) etc.

Inherited properties

The application should be keyed as a Purchase where:

- The property is not registered in the applicant's name e.g. the property is still registered in the name of the deceased, and there may or may not be a mortgage in the name of the deceased

or

- The applicant is a joint owner, but they need to purchase the remaining share due to a ‘Tenants in common’ restriction in place.

Examples of Purchase applications are:

- Where there are multiple beneficiaries and the applicant would like to buy them out

- Where the applicant wants to settle the deceased’s mortgage instead of selling the property. Additional lending may be required if also buying out other beneficiaries.

Submitting the application

The purchase price is the amount required to acquire full ownership of the property, for example:

- Property value: £100,000

- The applicant owns 50% share of the property and 50% is owned by the other beneficiary, therefore £50,000 is required to buy them out. Purchase price is therefore £50,000.

The application should be keyed as Remortgage application where there is a continuing owner:

- The property is registered in the applicant’s name

or

- The applicant is a joint owner with the deceased, and the property was held as joint tenants rather than tenants in common.

PEA Certificate / Reservation agreements

A Predicted Energy Assessment must:

- Display the title ‘Predicted Energy Assessment’

- Contain the following statement:

- ‘This document is a Predicted Energy Assessment for properties marketed when they are incomplete. It includes a predicted energy rating which might not represent the final energy rating of the property on completion. Once the property is completed, this rating will be updated, and an official Energy Performance Certificate will be created for the property. This will include more detailed information about the energy performance of the completed property.’

OR

- ‘This document is a Predicted Energy Assessment required to be included in a Home Information Pack for properties marketed when they are incomplete. It includes a predicted energy rating which might not represent the final energy rating of the property on completion. Once the property is completed, the Pack should be updated to include information about the energy performance of the completed property.’

- Contain the predicted asset rating of the building

- Contain the address or proposed address of the property.

If a PEA does not contain the address or proposed address of the property, request a ‘Plot Reservation’ form if not already provided by the customer.

A plot reservation form must:

- Contain the customer’s name

- Contain a suitable link to the PEA such as:

- House type

- Plot number

- PEA’s can be accepted if they are in draft format

There is no expiry date and can be accepted within any time frame.

Scottish property

Scottish properties should be processed in the same way as a discounted property by following the steps below:

- If a discount has been applied to the property by family members, relatives or any other individuals / firm, please select ‘Yes’ to this question.

- Loan to value, for policy, is linked to the ‘actual’ purchase price being paid to purchase the property. The customer’s minimum deposit must be in line with criteria linked to this LTV.

- The correct way to key this type of application is the following:

- Submit the case based on the actual market value of the property. This way, the valuation is instructed on the correct value and the correct rate can be selected.

- Upload an Application Amendment Form to change the purchase price to reflect the amount that the property is being purchased for. Please note, this needs to remain within policy limits for loan to value (LTV) etc.